My 2025 outlook focused on a set of major risks that the bull market faced, as well as what could keep driving the market to new highs.

That bull market was an equal-opportunity profit engine for investors. Until about 12 months ago. Here is how I look at it in snapshot form.

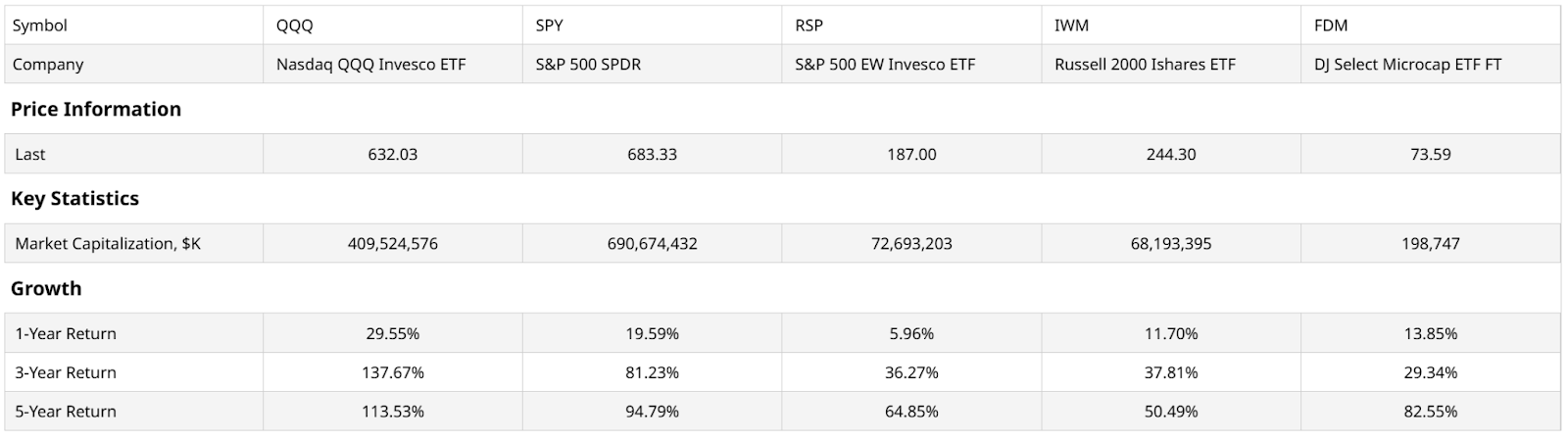

The Invesco Nasdaq 100 ETF (QQQ), which has been the leader of the stock market more often than not this century, went into overdrive in 2025. In the chart above, you can see it in the 1-year returns. While the S&P 500 Index ($SPX) has done well, it has done so essentially on the back of QQQ’s nearly 30% gain in 12 months, and a 3-year return among the best ever seen.

There’s a path for QQQ to rise another 30%, as that would follow the continued dot-com bubble era script. The year 2000 was when QQQ rose 75% and fell 75%. Both inside of a single calendar year! One reason I feel some of those same vibes has to do with the market’s current hyper-focus on AI stocks, like those leading the QQQ, and not much else.

However, when we strip out the rest of the stocks in the S&P 500, and look down the size spectrum, we see that the returns elsewhere have been solid, but lagging nonetheless. So, what’s the problem? That performance is in the past. And increasingly, I see signs that the market has entered that stage of the cycle where two things happen, in order:

- QQQ continues to plow higher, going farther than most could imagine, while the rest of the stocks start to roll over, segment by segment.

- QQQ, the leader, rolls over too. And the rest are not able to save it.

The Market Is Hanging on Thanks to QQQ and Not Much Else

The AI trade, like the dot-com trade 25 years ago, is one of those phenomena that will be life-changing, and profit-making. But perhaps not to the level of today’s lofty expectations. That means stock market gains can continue, but only for a little while longer. And only as long as the narrative doesn’t hit a speed bump.

In that outlook work I did about 10 months ago, I pointed out this concentration among the biggest stocks. This year, the rich have simply become richer. And the average stock in the S&P 500 is fading fast. So too are small caps, which have a world of hurt coming next year, as many of them face “debt cliffs” where they need to borrow to stay solvent.

This shows up in the smallest stocks, the so-called micro-caps, which are usually on fire when a “risk-on” mood persists. But by one benchmark in that table above, they have underperformed QQQ by a whopping 100% in the past 3 years. Wow. Just wow.

The market today is like an athlete playing on one good leg. They can perform well for a while, but at some point, the risk that performance tails off quickly is the likely scenario.

To me, in my own positioning, the whole trading plan revolves around QQQ. That is, I see that and not the S&P 500 as where the profits are. So that’s my base, hedged as I always am. And the “alpha” is sourced from most other areas of the U.S. stock market, by trying to profit from their decline.

How to Bet Against Small-Cap Stocks

That leads me to inverse ETFs like the Pro Shares Short Russell 2000 ETF (RWM), one I’ve used for decades. At this time of malaise in small-cap land, that makes sense to me to have close by at all times, to deploy if and when needed.

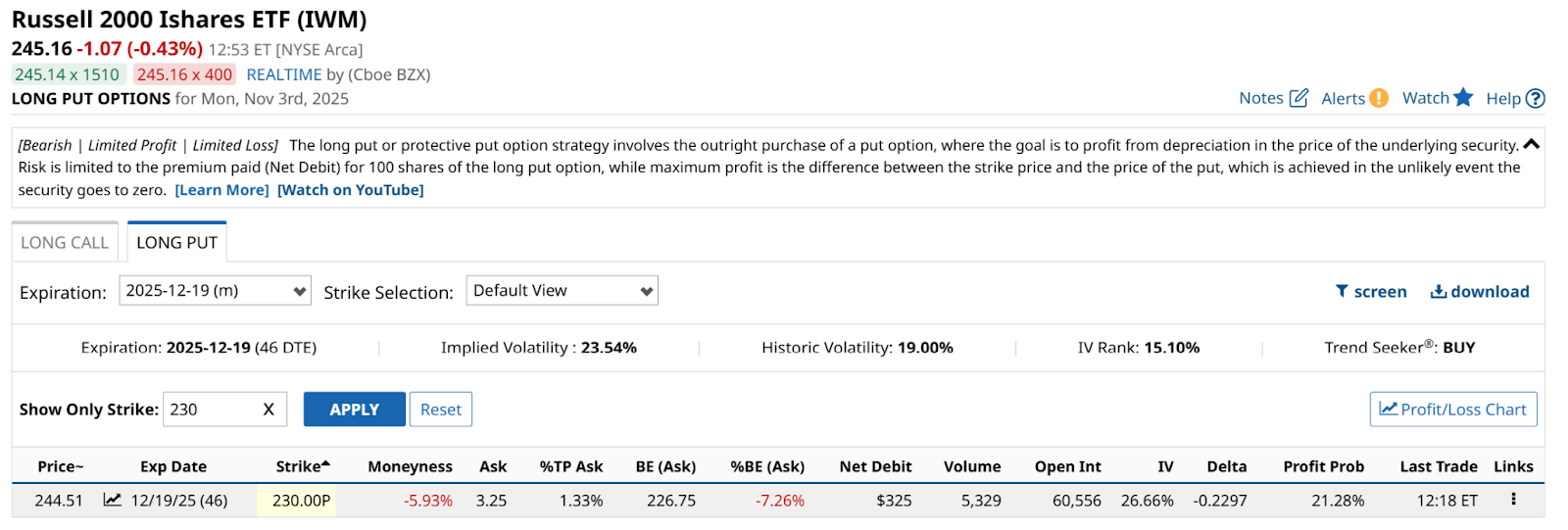

Put options on the Russell 2000 iShares ETF (IWM) are the same type of directional trade, but with the pros and cons of options: there’s a time limit, volatility impacts it both ways, and there’s a cost to get it started. Here’s an example.

IWM trades around $245 as of this writing. I can buy the right to sell 100 shares at $230 between now and Dec. 19. That’s about 6% below the recent price. It will cost me about 1% to put on this one, which is not bad considering that IWM’s “IV Rank” is 15%. That means it is toward the low end of its 12-month range.

The AI trade is alive and well. But when that fails to be the case, the next stage of the cycle is likely to be one that favors those who know how to play defense, not just offense.

Rob Isbitts, founder of Sungarden Investment Publishing, is a semi-retired chief investment officer, whose current research is found here at Barchart, as well as on Substack.

On the date of publication, Rob Isbitts had a position in: RWM , IWM . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart